Voluntary vs Involuntary Churn: Why Treating Them the Same Is Costing You Subscribers

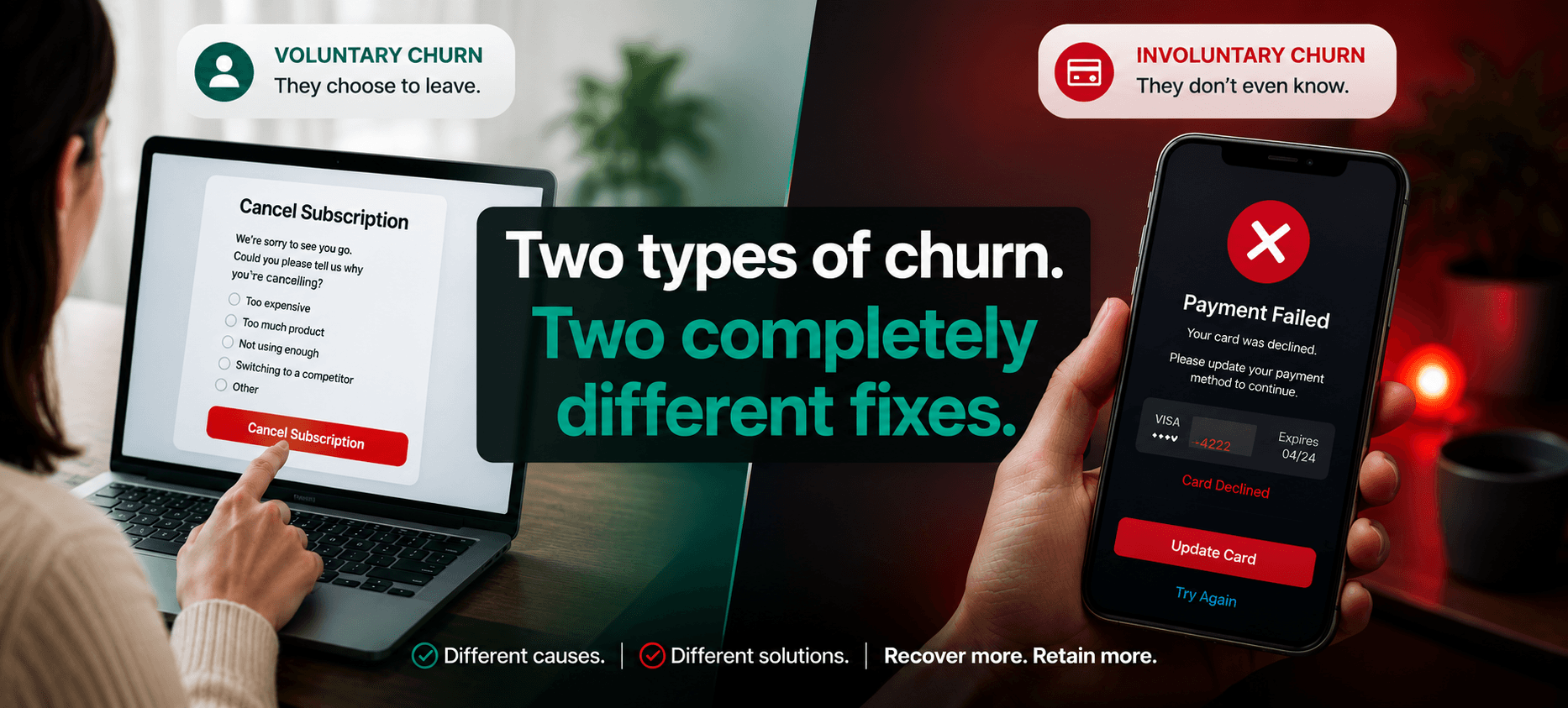

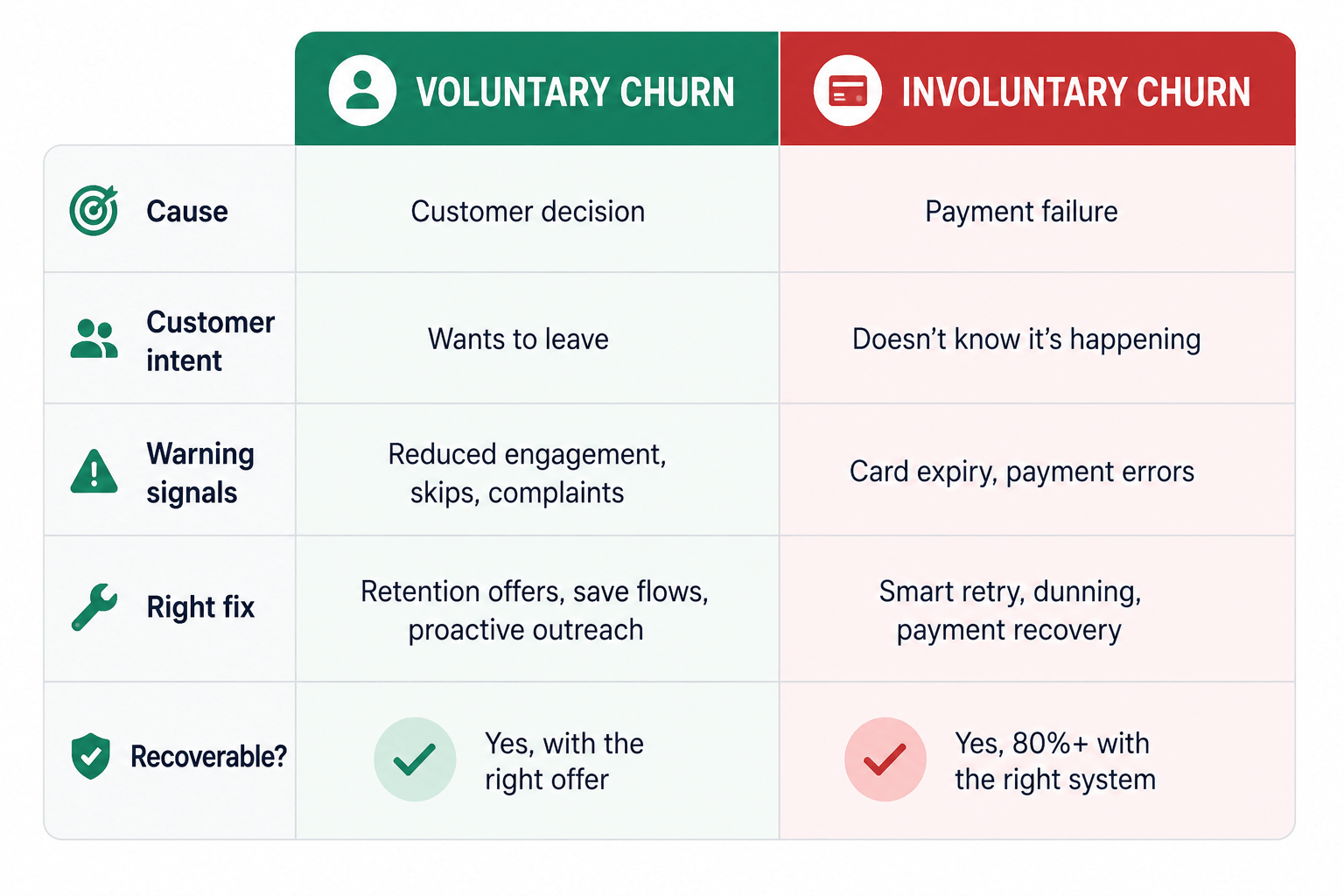

What is voluntary churn? Voluntary churn occurs when a subscriber actively chooses to cancel their subscription. Common reasons include finding it too expensive, accumulating too much product, losing interest, or switching to a competitor. It is a decision the customer makes and one that can often be intercepted with the right retention offer at the right moment.

What is involuntary churn? Involuntary churn happens when a subscriber loses access not because they want to leave, but because a payment fails, an expired card, insufficient funds, or a bank block. The customer has no intention of cancelling. The subscription simply stops because the billing infrastructure couldn’t complete the transaction.

Most subscription brands track a single churn number. One percentage. One dashboard metric. One thing to “reduce.”

The problem: that single number is hiding two completely different problems, and if you’re responding to both of them the same way, you’re solving neither.

Voluntary and involuntary churn have different causes, different signals, and different fixes. Lumping them together doesn’t just muddy your analytics but actively costs you subscribers you could have kept.

Voluntary vs Involuntary Churn: The Numbers Behind the Split

Involuntary churn, the kind caused by failed payments, accounts for anywhere from 20% to 40% of total subscription churn, depending on the industry and subscriber base. For Shopify subscription brands specifically, that number tends to sit in the 30–40% range.

That means for every 10 subscribers you “lose” in a month, 3 to 4 of them didn’t actually want to leave. Their card failed. Your platform retried on a fixed schedule. It failed again. Their subscription got cancelled. They probably didn’t even notice until their next order didn’t arrive.

According to Recurly’s 2026 State of Subscriptions report, failed payments are consistently one of the top two drivers of subscriber loss across subscription businesses. The majority of those failures are recoverable with the right recovery approach applied at the right time.

Industry digital payments research also continues to highlight how payment failures, card lifecycle events, and authentication requirements remain persistent challenges for merchants managing recurring billing.

Meanwhile, voluntary churn, the kind where a subscriber deliberately hits “cancel”, is driven by something entirely different: perceived value, affordability, product fit, or simple life changes. No amount of smart payment retries will fix a customer who feels your product is too expensive. And no amount of personalised retention offers will help a customer whose card has genuinely expired.

Why the Confusion Happens

Most subscription management platforms don’t separate these two churn types clearly in their dashboards or in their response logic.

A customer whose card fails gets the same dunning email as everyone else. A customer who clicked cancel because they had too much product gets the same “are you sure?” screen as someone who thinks the product is too expensive. There’s no distinction. No tailored response.

This creates two failure modes:

Failure mode 1: You try to “retain” customers who aren’t actually trying to leave. Sending a discount email to someone whose card failed doesn’t help them — it just adds noise before their subscription gets cancelled anyway.

Failure mode 2: You miss the real intervention window for customers who are genuinely at risk. A customer who’s been skipping orders for two months isn’t going to respond to a generic pause offer. They need a personalised outreach before they reach the cancellation page at all.

Both failure modes mean lost recurring revenue. And both are avoidable.

Why Subscription Businesses Need Separate Strategies for Each Type of Churn

Most subscription businesses eventually discover that reducing churn isn’t about finding a single solution; it’s about solving two fundamentally different problems. Voluntary churn is driven by customer decisions, requiring proactive engagement, personalised retention offers, and meaningful cancellation experiences. Involuntary churn is caused by payment failures and billing issues, making payment recovery, smart retries, and card update workflows the priority. Treating both with the same automation often creates unnecessary friction and leaves recoverable revenue behind. The most effective subscription retention strategies separate these workflows while allowing them to share subscriber context.

Fixing Voluntary Churn: The Retention Side

Voluntary churn has two intervention windows, and most brands only address one of them.

Window 1: Before the customer decides to cancel. This is where proactive customer retention makes its impact. Subscribers who are disengaging (skipping orders, reducing quantities, opening emails less) are showing signals weeks before they ever reach the cancel button. Catching them here, when you still have leverage, is significantly more effective than trying to convince them at the exit door.

This approach also aligns with broader customer experience research from the Baymard Institute, which shows that reducing friction and addressing customer concerns early leads to better long-term engagement and retention than relying solely on end-stage interventions.

Window 2: At the moment of cancellation. When a customer does hit cancel, the reason they give matters. “Too expensive” calls for a discount. “Too much product” calls for a skip or a frequency change. “Need a break” calls for a pause. A generic retention popup that shows the same offer to every cancellation reason isn’t a save flow; it’s a checkbox.

For a full picture of how the first 90 days shape long-term voluntary churn, see our post on why 44% of cancellations happen in the first 90 days and what to do about it before subscribers ever reach the cancel button.

Fixing Involuntary Churn: The Recovery Side

Involuntary churn is, in many ways, the easier problem to fix if you have the right system. The customer wants to stay. You just need to resolve the billing issue before they even realise there’s a problem.

Where most platforms fall short: they treat all payment failures the same. Retry on day 3. Retry on day 7. Send a generic “please update your payment” email. Cancel on day 14.

But a card that failed due to insufficient funds and a card that’s been reported stolen require completely different responses. Retrying a cancelled card is a waste of billing attempts and can flag your account with payment networks. Sending a “please update your card” email to a customer who just had a temporary bank block is unnecessary friction.

Industry recovery benchmark data consistently shows that failure-type classification is one of the biggest drivers of payment recovery improvement. When you know why a payment failed, you know what to do next.

We covered the full recovery sequence in detail in the blog, 85% of failed payments are recoverable — here is the recovery sequence that gets them back, including how timing, channel selection, and failure classification combine to drive recovery rates that generic dunning simply can’t match.

Why Payment Recovery and Churn Prevention Must Work Together

Here’s where the two-problem framing gets important for your platform choice: voluntary and involuntary churn aren’t just different problems. They actively overlap.

A subscriber with a payment in recovery is also a subscriber at elevated churn risk. If you’re running a separate churn-prevention system that doesn’t account for open payment cases, you risk sending a re-engagement offer to someone already frustrated by a billing failure, doubling down on friction instead of resolving the actual issue.

Similarly, a subscriber who reaches the cancellation flow during a payment dispute needs a different retention response than one who’s cancelling because they think your product is too expensive.

This is why connected systems, where payment recovery, proactive churn prevention, and cancellation save flows share context, outperform stacked tools that don’t know what the other is doing. It’s also why the gap between average recovery rates and what’s genuinely achievable tends to be widest for brands relying on disconnected point solutions.

Learn why disconnected retention tools often leave recovery gaps in our guide to AI replacing traditional subscription retention tools.

For a broader look at how AI changes the economics of subscriber retention strategy across both churn types, see the Complete Guide to Subscription Retention & Revenue Recovery.

When payment recovery, churn prevention, cancellation saves, and winback campaigns work together, brands can deliver more relevant customer experiences, recover more recurring revenue, and make better retention decisions across the entire subscriber lifecycle.

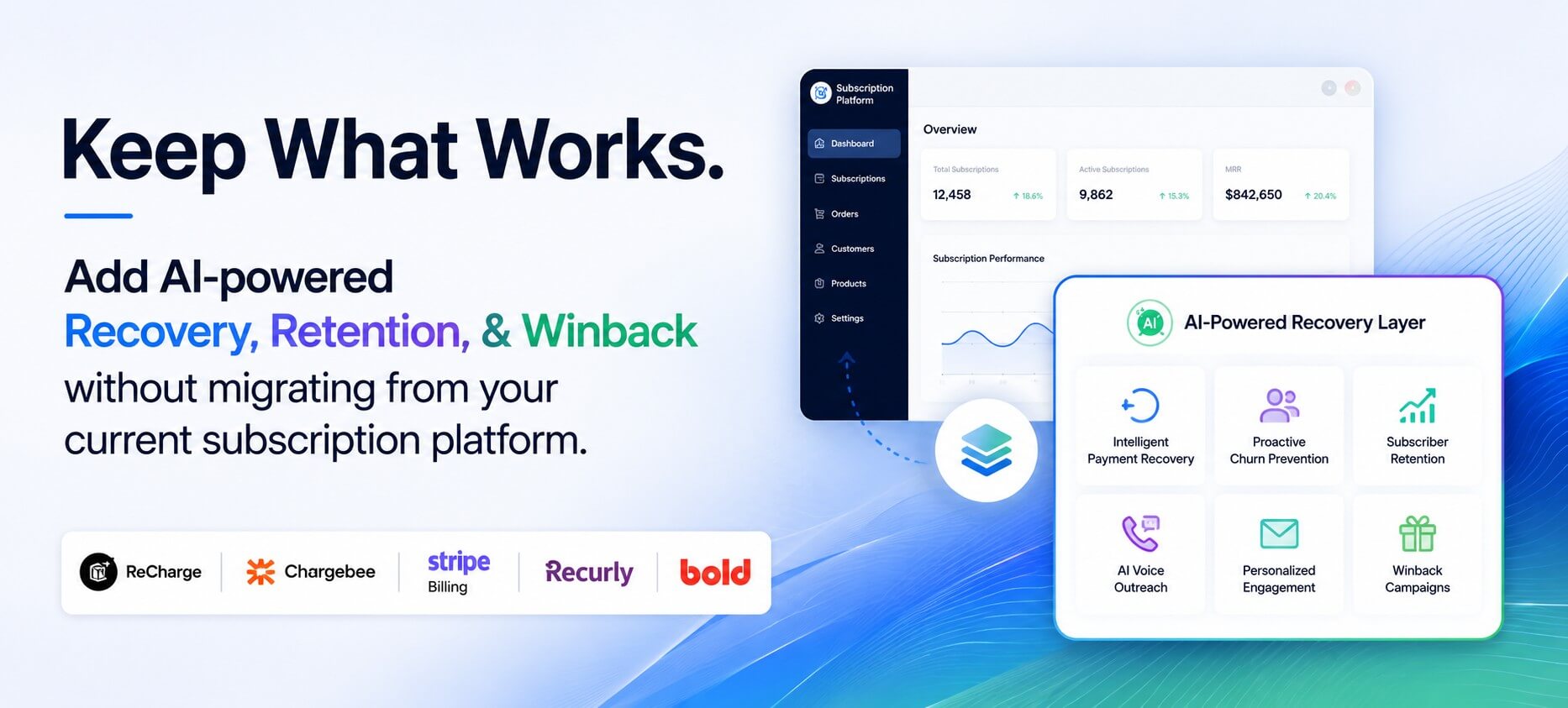

What enComm Does Differently

enComm treats voluntary and involuntary churn as separate problems with dedicated systems for each that share subscriber context.

On the involuntary side: every failed payment is classified by type before any action is taken. Soft declines are retried at intelligently timed windows. Hard declines go straight to card update outreach, no wasted retries. Customers whose banks require authentication get a message that actually explains SCA, not a generic “please update your card” email. Recovery plans are tailored to each subscriber’s payment situation and engagement history, helping brands deliver more relevant recovery experiences.

On the voluntary side: the proactive churn prevention system continuously identifies subscribers showing early signs of churn risk. High-risk subscribers receive outreach and, where appropriate, a targeted retention offer, before they ever reach the cancellation page. When a customer does try to cancel, the save flow reads their reason and responds with the offer most likely to work. If the first offer is declined, a second, different offer is presented. The system tracks what’s been offered before, so the same customer is never shown the same offer twice.

And critically: both systems share context. A subscriber in active payment recovery is excluded from churn interventions. A subscriber who declined a discount during cancellation won’t receive the same discount in a winback campaign.

The Takeaway

Voluntary and involuntary churn look the same in your churn rate metric. They don’t behave the same, they don’t have the same causes, and they don’t respond to the same fixes.

Treating them the same is the most common and most expensive mistake brands make with their subscription retention strategy.

The brands with the highest subscriber retention rates aren’t just running better offers. They’re running separate, intelligent systems for each churn type, systems that know what kind of churn they’re dealing with before deciding what to do about it.

Want to see how enComm handles the complete customer lifecycle? Explore the Complete Guide to Subscription Retention & Revenue Recovery.

Frequently Asked Questions

Voluntary churn happens when a subscriber actively chooses to cancel their subscription because of price, product fit, or changing needs. Involuntary churn happens when a subscriber loses their subscription due to a payment failure, not a deliberate decision to leave. The subscriber often doesn’t know the cancellation happened until their next order doesn’t arrive.

Industry research places involuntary churn at 20–40% of total subscription churn, with most Shopify subscription brands experiencing it in the 30–40% range. This means a significant portion of every brand’s “lost” subscribers didn’t actually want to leave. They were lost to payment failure.

Yes. The majority of involuntary churn is recoverable when handled with the right system. The key is classifying the failure type correctly, distinguishing between a temporary issue that can be retried versus a card that needs to be replaced and executing the right recovery action for each case. Brands using intelligent recovery systems consistently recover the large majority of involuntary churners.

The most common causes are expired or cancelled cards, insufficient funds at the time of billing, daily spending limit blocks, bank authentication requirements, and technical payment processing errors. Each cause requires a different response.

Voluntary churn reduction works at two stages: before the cancellation decision (through proactive outreach to at-risk subscribers) and at the moment of cancellation (through personalised save offers matched to the reason the customer is leaving). Generic retention offers or single-option save flows significantly underperform compared to reason-matched, two-round negotiation approaches.

Early signals include declining email engagement, increased order skips, product quantity reductions, and subscription modification activity. Brands using daily churn risk scoring, which combines these signals into a single risk score per subscriber, can identify at-risk subscribers weeks before they reach the cancellation page, when intervention is most effective.

Both require fundamentally different responses. A subscriber whose card failed needs billing recovery support, smart retries, card update requests, and authentication links. A subscriber who’s thinking about cancelling needs re-engagement, value communication, or a tailored retention offer. Sending retention offers to payment-failed subscribers adds confusion. Sending dunning emails to someone who’s disengaged doesn’t address why they’re at risk. The systems need to be distinct, but they also need to share subscriber context so neither creates conflicting outreach.

Although voluntary churn often receives more attention, involuntary churn can account for 20–40% of subscriber loss. Because many of these customers still want to remain subscribed, improving payment recovery can recover revenue without acquiring new customers.

Proactive churn prevention identifies subscribers showing early signals of disengagement and reaches out to them with personalised re-engagement messaging or retention offers before they’ve decided to cancel. This is distinct from reactive save flows that only trigger when a customer initiates a cancellation. Proactive prevention is consistently more effective because intervention happens when there’s still leverage.

Yes. enComm’s platform includes separate systems for both: an AI-powered payment recovery engine for involuntary churn (with failure classification, smart retry timing, multi-channel outreach, and AI voice calls) and a proactive churn prevention and intelligent cancellation save flow system for voluntary churn. Both systems share subscriber context so outreach is never conflicting or redundant.