85% of Failed Payments Are Recoverable — Here Is the Recovery Sequence That Gets Them Back

Failed payments don’t have to mean lost revenue. The question is whether your recovery system is built to actually fix them or just send a generic “please update your card” email and hope for the best.

There’s a number that tends to surprise Shopify subscription merchants when they first hear it: research from the payments industry consistently shows that the majority of failed subscription payments, often cited at 70–85%, are recoverable with the right intervention at the right time.

The reason most brands don’t recover them isn’t that the customers don’t want to stay subscribed. It’s that the recovery system treats a card that’s been reported stolen the same way as a card that temporarily hit its daily spending limit. It’s retrying a permanently invalid card four times before anyone thinks to ask the customer for a new one. It’s sending a dunning email at 2 a.m. on a Saturday when the customer is asleep, and their account balance is lowest.

Recovery isn’t just about trying harder. It’s about trying smarter, matching the response to the specific failure, and timing everything around the individual customer’s actual situation.

This post explores the principles behind effective failed payment recovery, including why payment failures should be treated differently, how recovery strategies can adapt to the subscriber, and how multiple engagement channels work together to reduce involuntary churn.

Key Takeaway

Most failed subscription payments are not lost revenue. Recovery rates improve significantly when payment failures are identified correctly, recovery actions match the underlying issue, and subscriber outreach is timed and personalized appropriately.

Related reading: If you’re still unclear on the difference between payments failing and customers choosing to leave, start with Why 30–40% of Your Subscriber Churn Is Actually Involuntary — it sets the context for everything in this post.

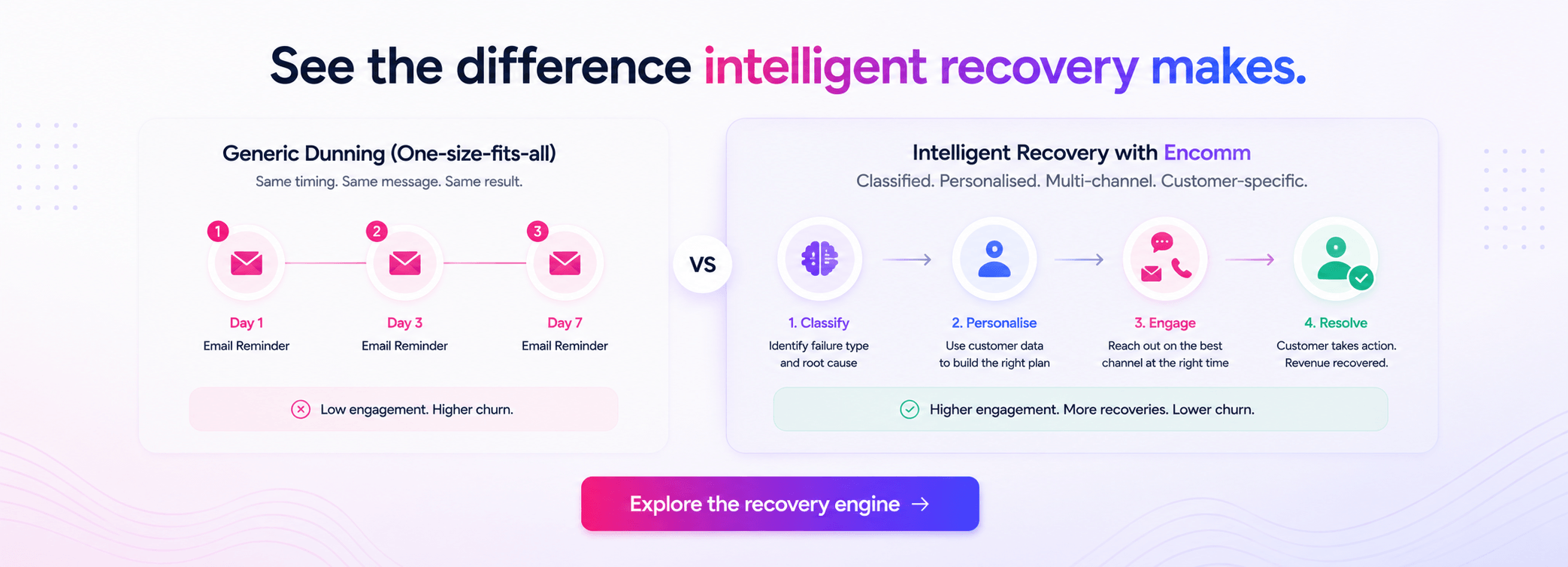

Why Most Failed Payment Recovery Sequences Fail Before They Start

The fundamental problem with standard dunning is that it’s uniform. Every failed payment goes into the same queue, gets the same retry schedule, receives the same email template, and is written off on the same day if nothing works.

This uniformity is the problem because not all payment failures are created equal.

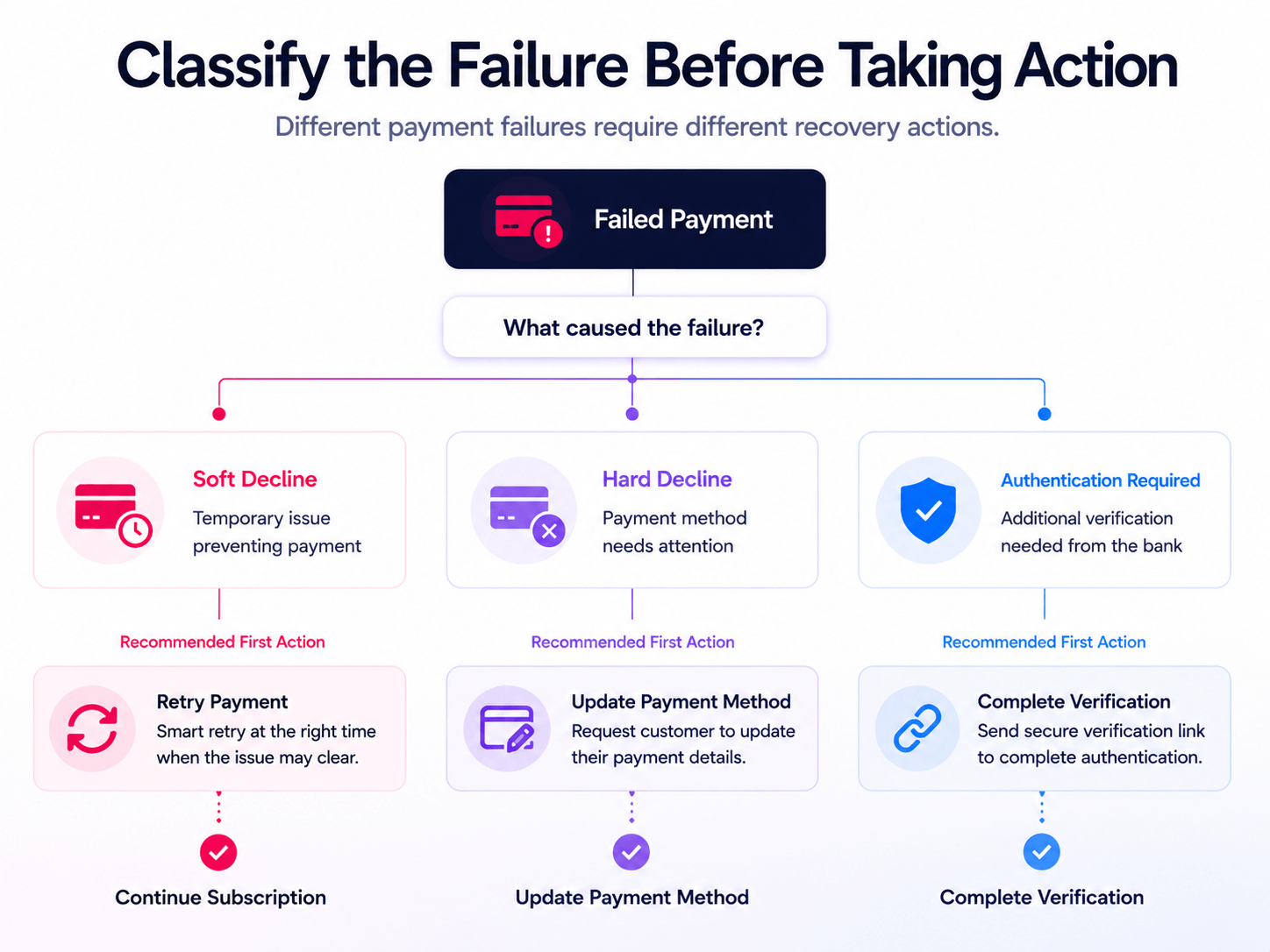

A soft decline — something like insufficient funds, a daily spending limit being reached, or a bank velocity block — is temporary. The card is valid. The customer intends to pay. The right response is a well-timed retry when their account is likely to have cleared.

A hard decline — an expired card, a cancelled card, one reported lost or stolen — is permanent. No number of retries will succeed. The only path forward is getting the customer to update their payment method. Every retry you run on a hard-declined card is a wasted attempt that can also hurt your standing with payment networks.

An authentication-required failure, common under European SCA/PSD2 regulations, is neither of the above. The card is valid and the customer wants to pay, but their bank is requiring them to authenticate the transaction. Sending them a “please update your card” email is actively confusing — they don’t need to update anything, they need to complete an authentication step.

When your recovery system treats all three of these situations identically, you’re already losing recoverable revenue before a single email goes out.

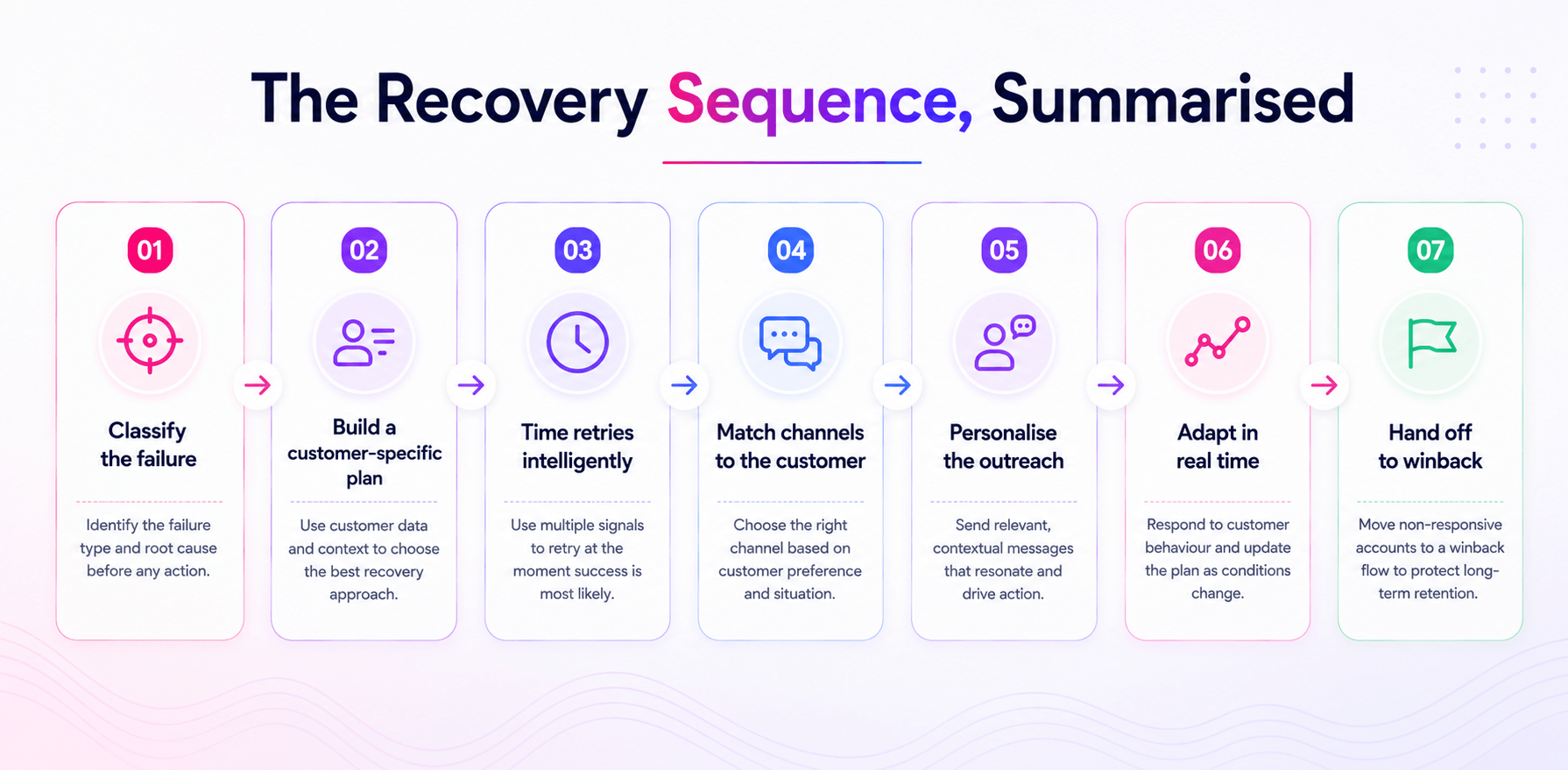

Step 1: Classify the Failure First — Before Anything Else

The first step in any effective recovery sequence isn’t outreach. It’s classification.

Before the system retries anything or contacts anyone, it needs to understand what actually went wrong. This means reading the error code and message returned by the payment gateway and categorising the failure accurately.

For standard, well-documented error codes, this is straightforward — a card expiry error is a hard decline, an NSF error is a soft decline. But a meaningful proportion of payment failures return ambiguous or non-standard codes that don’t map cleanly to either category. In these cases, AI analysis of the raw error message — interpreted in context — produces a classification with a confidence score and a plain-English rationale.

This classification step takes seconds and runs before any other action. It’s what prevents the system from:

- Retrying a hard decline repeatedly (wasting attempts and flagging your account)

- Sending a card-update email to someone who just needs to complete a bank authentication step

- Treating a velocity block the same way as an account closure

Get classification right, and everything downstream — retries, outreach, channel selection — starts from accurate information.

Step 2: Build a Recovery Plan Specific to This Customer

Once the failure is classified, the recovery system should do something that most platforms don’t: read the customer’s profile before deciding how to reach them.

Recovery strategies should reflect subscriber context rather than treating every failed payment identically. Factors such as subscriber tenure, customer lifetime value, engagement history, payment behaviour, and available communication channels & preferences can all influence the most appropriate recovery approach.

Different subscriber profiles often benefit from different recovery strategies. The goal is not to increase outreach volume, but to select the most appropriate recovery actions based on the specific circumstances of each subscriber. A well-built recovery system selects from a library of recovery patterns, each one a different combination of channels, timings, and conditions, and builds a concrete plan before any outreach begins.

Step 3: Time Retries for When They’re Most Likely to Succeed

Effective retry timing takes into account multiple variables, including the reason for the payment failure, the subscriber’s payment history, local banking behaviour, and previous recovery outcomes. Rather than relying on fixed schedules, modern recovery systems adapt retry timing based on contextual signals that increase the likelihood of success.

Smart retry timing draws on several signals simultaneously:

Failure subtype — NSF failures align with typical paydays; velocity blocks wait for the block reset; network-level failures use progressive backoff that avoids repeating the same attempt too quickly.

The customer’s own billing history — if a customer has successfully charged on the 1st and 15th of every month for the past year, that pattern is relevant. Their typical successful payment window is better evidence than any generic schedule.

Country and banking conventions — different countries have different payroll and credit cycles. A subscriber in the UK, Germany, India, and Australia each has different banking calendars, and retry timing should account for them.

Customer timezone — retries scheduled at 10 a.m. local time align with overnight account credits and typical online banking activity windows.

Day-of-week preference — payment networks show measurably higher success rates Tuesday through Thursday. Avoiding Monday and Friday isn’t superstition; it’s pattern data.

Anti-velocity guard — regardless of everything else, never retry within 18 hours of the previous attempt. Retrying too quickly triggers issuer velocity blocks that make subsequent attempts harder, not easier.

Step 4: Match the Outreach Channel to the Customer

For hard declines and cases where soft decline retries haven’t succeeded, outreach is necessary. But “outreach” shouldn’t mean sending a templated email and waiting.

The channel, the timing, and the sequence of channels should be selected based on the customer’s actual engagement history and the contact methods available.

For a high-value customer with a hard decline: The most effective approach is parallel outreach, with an email with a secure payment update link sent at the same time as an SMS, followed by an AI outbound call if neither has prompted action. Speed matters for high-value customers. The relationship is worth more, and the urgency of early action reflects that.

For a customer with a hard decline and low email engagement: An email is unlikely to move them. An SMS followed by an early AI call maximises reach for someone who historically doesn’t open emails.

For a customer with a soft decline who regularly opens your emails: Smart-timed retries with conditional email outreach is the appropriate path. No phone call needed. No SMS. Just the right message at the right time.

For a customer with no phone number, no SMS opt-in, and AI calling disabled: Email-only sequence. The system should adapt to what’s actually available rather than treating every case as if every channel exists.

The objective isn’t to use more channels but to reach subscribers through the channels most likely to drive action rather than applying the same communication sequence to every case.

Step 5: Use Outreach That Actually Addresses the Situation

The content of your outreach matters as much as the timing and channel.

A two-year subscriber whose card expired deserves a different message than a two-month subscriber who hit an NSF failure. The expiry message should acknowledge the relationship, remind them of the value they’d lose, and make it easy to update — one click, no login required. The NSF message needs a different tone and a different framing.

When outreach copy is generated specifically for the individual case ( using the customer’s name and product, the actual failure reason, the recovery action needed, and whether this is the first, second, or final message in a sequence) then acceptance rates are meaningfully higher than when the same template goes to everyone.

The same principle applies to AI outbound phone calls. AI voice interactions are most effective when they have sufficient context about the subscriber and the recovery situation. In enComm, the AI agent enters the call with full context about the customer, recovery attempts, past retention offers, etc. It can also send a secure payment update link to their phone during the call, answer questions about their subscription, and offer a retention deal if appropriate.

For customers who don’t read emails and don’t respond to SMS, AI calls are often the recovery channel that closes the case. According to 2025 payment benchmarks from The Kaplan Group, personalised and contextualised outreach, matched to the failure reason and customer segment, is one of the key drivers separating best-in-class recovery rates of 70–85% from the industry median of around 47%.

Step 6: Let Plans Adapt in Real Time

A recovery plan that runs on a fixed rail (executing each step regardless of what has happened since the last one) generates unnecessary friction and wastes outreach on customers who’ve already acted.

Plans should adapt automatically as events occur: When a customer updates their payment method, all remaining outreach steps should pause immediately, and a confirmatory retry should run. The customer shouldn’t receive a follow-up SMS for an issue they already resolved.

Effective recovery systems continuously adapt as new subscriber actions occur. Recovery workflows should respond dynamically to email hard bounce, payment updates, engagement signals, communication preferences, opt-outs, and resolution events, ensuring subscribers receive relevant outreach while avoiding unnecessary contact.

Recurly’s 2026 State of Subscriptions report, drawing on data from 76 million subscribers, found that the software industry alone recovered over $155 million in revenue through payment recovery tools in 2025, underscoring that adaptive recovery sequencing isn’t a marginal improvement; it’s a material revenue lever.

Step 7: Know When to Hand Off to Winback

Not every case will resolve through the automated recovery sequence. Some customers update their card only after cancelling. Some don’t respond to any outreach before the recovery window closes.

For customers whose subscriptions are cancelled as a result of a failed payment, rather than choosing to leave, a post-cancellation winback campaign gives you a second chance. The key difference from a voluntary cancellation winback is that these customers didn’t intend to leave. The barrier to reactivation is lower. The right offer and the right timing can bring a meaningful percentage back.

For customers who cancelled involuntarily, an early email with a clear reactivation link and an honest acknowledgement of what happened tends to perform better than a generic “we miss you” message sent weeks later.

How This Connects to Your Broader Retention Strategy

Payment recovery doesn’t exist in isolation. The most effective subscription businesses treat failed payments and voluntary cancellations as two parts of the same problem — revenue leaving the business — and make sure the systems handling both share context.

A customer with an open payment recovery case shouldn’t also be receiving proactive churn outreach that competes with or contradicts the recovery messaging. A customer who received and declined a discount offer during their cancellation flow shouldn’t be offered the same discount as their first winback step.

For a broader look at how these systems work together, the Complete Guide to Subscription Retention & Revenue Recovery for Subscription Brands covers the full picture, from proactive churn prevention to voluntary cancellation saves to post-cancellation winback.

And if you’re thinking about the long-term revenue impact of getting recovery right, see how the numbers compound in our breakdown of how AI-engaged customers achieve 40–60% higher 12-month CLV.

The difference between recovering 30% of failed payments and recovering 70–80% isn’t effort. It’s intelligence applied at every step — from the moment a failure comes in to the moment the case closes. If you want to see how this plays out across the full subscription lifecycle — and how recovery connects to proactive churn prevention How AI Orchestration Replaces 5 Separate Shopify Apps is worth reading next.

Frequently Asked Questions About AI Voice Payment Recovery

Industry data consistently shows that the majority of failed subscription payments, typically cited in the range of 70–85%, are recoverable with the right intervention. The key variables are how quickly the recovery attempt starts, whether the failure type is correctly identified, and whether outreach timing is matched to the customer’s actual payment patterns.

A soft decline is a temporary failure. The card is still valid, but the charge failed for a time-limited reason such as insufficient funds, a daily spending limit being reached, or a bank velocity block. A smart retry at the right time will typically succeed. Whereas a hard decline is permanent failure. The card is expired, cancelled, reported lost or stolen, or flagged for fraud. No retry will succeed; the customer must provide a new payment method.

For soft declines, the right number of retries depends on the failure subtype and how long the customer typically takes to clear their account. What matters more than the count is the timing of each attempt. For hard declines, retrying is counterproductive — the energy should go immediately into prompting a card update.

Customers who don’t engage with email may respond to SMS or, particularly for high-value subscribers, an AI outbound phone call. A well-structured recovery sequence escalates through channels based on engagement history, not on a fixed schedule. Customers who have never opened a recovery email shouldn’t receive four of them before any other channel is tried.

When calls are placed with full context and when it can resolve the issue in a single conversation, most customers find them efficient rather than intrusive. The key is placing calls during appropriate hours in the customer’s local timezone, limiting the number of attempts, and ensuring the call respects opt-out requests immediately.

This depends on the failure type and the customer profile. For soft declines, recovery typically runs for 7–14 days. For hard declines, the window is open-ended until the customer updates their payment method, though outreach intensity tapers. The sequence should stop automatically the moment the issue resolves, regardless of how many steps remain.

They’re two sides of the same problem: subscribers leaving the business. The most effective approach treats them as connected. A customer with an open payment recovery case shouldn’t also be receiving separate churn prevention outreach, and a customer who declined a retention offer during cancellation shouldn’t receive the same offer again in a winback sequence. Systems that share context perform better than systems that operate in silos.

Most subscription brands recover failed payments through a combination of payment retry optimization, personalized customer outreach, and multi-channel engagement. Modern recovery systems use contextual signals to determine the best recovery strategy for each subscriber, helping reduce involuntary churn and protect recurring revenue.